In the fast-moving UK financial market, short-term borrowing has evolved significantly. While many traditional payday lenders have disappeared, Fernovo loans have established a reputation as a modern, technology-driven alternative for those needing a quick bridge to their next payday.

If you are considering an application for Fernovo loans in 2026, it is essential to understand how their “Novo-Quote” technology works, the costs involved, and how they compare to other lenders in the UK. This comprehensive guide covers everything you need to know.

What are Fernovo Loans?

Fernovo loans are short-term instalment loans provided by Quidie Limited, a direct lender authorized and regulated by the Financial Conduct Authority (FCA). They specialize in “quick cash” solutions, typically ranging from £300 to £1,500, with repayment terms spread over 3 to 6 months.

The brand is built on three pillars: speed, transparency, and manual underwriting. Unlike some competitors who rely solely on automated algorithms that might reject you for a minor blip on your credit report, Fernovo uses a “Novo-Quote” system to provide a real-time decision without initially impacting your credit score.

Key Features of Fernovo:

-

Loan Amounts: Up to £1,000 for new customers; up to £1,500 for returning customers.

-

Repayment Terms: Flexible terms between 3 and 6 monthly instalments.

-

Interest Cap: In line with FCA rules, interest is capped at 0.8% per day.

-

Direct Lender: You deal with Fernovo directly—there are no middleman fees.

How Fernovo Loans Work: The “Novo-Quote”

One of the standout features of Fernovo loans is their proprietary Novo-Quote system. This technology addresses the primary fear of UK borrowers: “Will applying for this loan damage my credit score?”

-

The Soft Search: When you first provide your details, Fernovo performs a “soft” credit search. This allows them to see if you are eligible and provide a quote without leaving a footprint that other lenders can see.

-

The Manual Review: Once you decide to proceed, Fernovo’s credit analysts manually review your application. This human element often helps people with “fair” credit get approved where automated systems might say no.

-

The Hard Search: A “hard” footprint is only added to your credit file if you successfully receive the loan.

Eligibility Criteria for Fernovo Loans

To apply for Fernovo loans in the UK, you must meet several baseline requirements:

-

Age: You must be between 18 and 67 years old.

-

Residency: You must be a permanent resident of the UK.

-

Employment: You must be employed and have a minimum take-home salary of £1,250 per month.

-

Banking: You must have a UK bank account with a valid debit card and a mobile phone for verification.

Understanding the Cost: APR and Daily Interest

When borrowing from high-cost, short-term lenders like Fernovo, it is vital to understand the Total Amount Repayable. As of April 2026, Fernovo loans carry a Representative APR of approximately 1,250% – 1,300%.

While this number looks high compared to a mortgage or car loan, it reflects the short-term nature of the product. The most important figure for most borrowers is the daily interest rate, which is 0.8%.

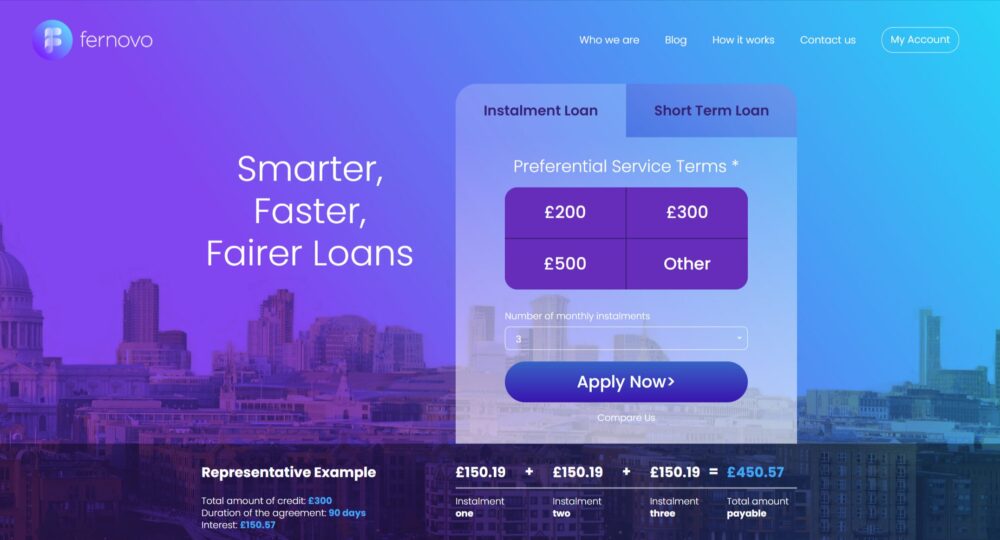

Representative Example (2026):

Amount Borrowed: £300

Term: 3 Months (90 days)

Interest: £150.57

Total Repayable: £450.57

Repayment Amount: 3 monthly payments of £150.19

Note: There are no hidden fees. If you pay your loan back early, you only pay the interest for the days you actually had the money.

Customer Reviews and Reputation

As of early 2026, Fernovo loans maintain an “Excellent” rating on Trustpilot, with over 7,000 reviews and a score of 4.5/5.

Common praise includes:

-

Speed: Many customers report funds arriving in their bank account within minutes of the manual review being completed.

-

Communication: Clear reminders via email and text before payment dates.

-

Support: Reviewers often mention the helpfulness of the “customercare@fernovo.co.uk” team when they need to adjust a payment date.

Common criticisms:

-

Declines after Quote: Because they use manual underwriting, some customers are declined at the final stage even if the soft search was positive.

-

Strict Income Requirement: The £1,250 monthly salary floor is higher than some other short-term lenders.

Comparison: Fernovo vs. Other UK Lenders

| Feature | Fernovo Loans | QuidMarket | Drafty (Line of Credit) |

| Max Loan | £1,500 | £1,500 | £3,000 |

| Search Type | Soft (Quote) | Hard (usually) | Soft (initial) |

| Approval Method | Manual Review | Manual Review | Automated |

| Early Repay Fee | £0 | £0 | £0 |

| Repayment Term | 3 – 6 Months | 3 – 6 Months | Flexible |

Is a Fernovo Loan Right for You?

Fernovo loans are specifically designed for emergency, short-term needs. They are a good fit if:

-

You have an unexpected expense (like a car repair) that cannot wait until payday.

-

You want a lender that looks at your actual affordability, not just a credit score.

-

You intend to pay the loan back within a few months.

They are NOT suitable if:

-

You are looking for a long-term solution to debt.

-

You are borrowing to pay off other short-term loans (this can lead to a debt spiral).

-

Your income is below £1,250 per month.

Fernovo Loan Summary and Final Verdict

In 2026, Fernovo loans remain one of the most trusted names in the UK’s high-cost, short-term credit market. Their commitment to manual underwriting and “soft search” quotes makes them a borrower-friendly choice for those with less-than-perfect credit.

However, the cost of credit is high. Before applying, always explore cheaper alternatives, such as your local Credit Union or a Budgeting Advance if you are on benefits. If you do choose Fernovo, their transparent “no hidden fees” policy ensures that as long as you pay back on time, you know exactly what the cost will be.

Financial Help: If you are struggling with debt, you can get free, confidential advice from MoneyHelper, StepChange, or Citizens Advice.