In the fast-paced world of UK financial services, finding a flexible alternative to traditional banking can be a game-changer. One of the most prominent names to emerge in the “alternative credit” space is Drafty loans.

Unlike standard fixed-term loans or restrictive payday lenders, Drafty offers a unique approach to borrowing. In this comprehensive guide, we will explore how Drafty loans work in 2026, their key features, and whether they are the right fit for your financial toolkit.

What are Drafty Loans?

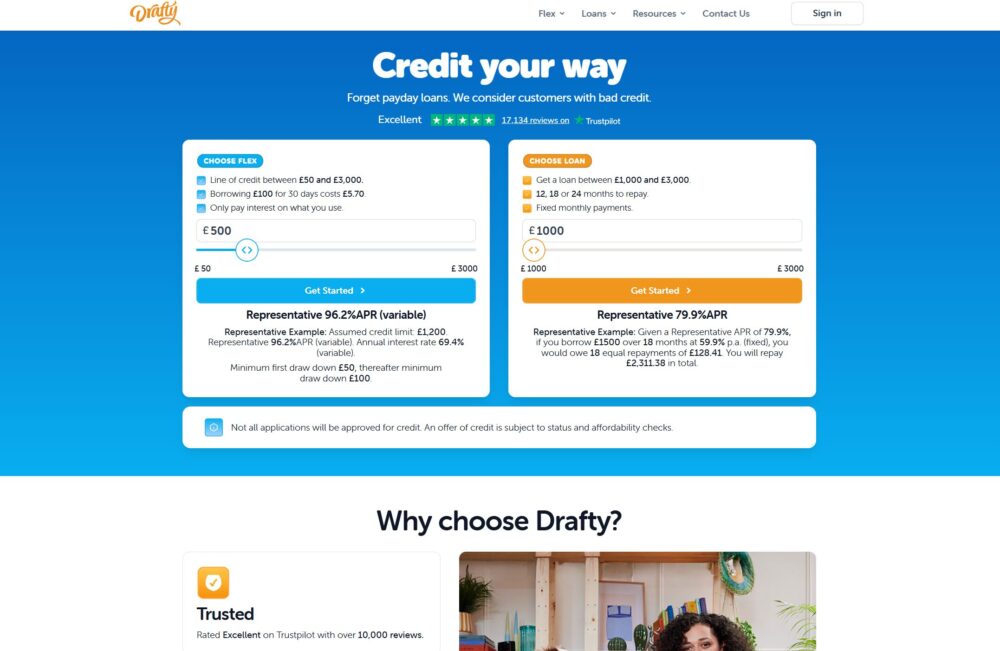

Strictly speaking, Drafty loans are not always “loans” in the traditional sense. While they do offer personal instalment loans, they are most famous for their Flexible Line of Credit.

A line of credit functions more like a credit card or a reusable pot of cash. Instead of receiving a lump sum and paying it back over a fixed period, you are given a credit limit (up to £3,000). You can “draw down” money whenever you need it, and you only pay interest on the amount you have actually used.

Key Features of Drafty:

-

Credit Limits: Typically between £50 and £3,000.

-

Speed: Approved funds can often reach your UK bank account in under 90 seconds.

-

Daily Interest: You are charged a daily interest rate (approx. 0.19% variable), meaning if you borrow for three days, you only pay for three days.

-

No Hidden Fees: Drafty is well-known for its “no fee” policy—there are no arrangement fees, no late payment fees, and no early repayment penalties.

How Drafty Loans Differ from Payday Loans

For many years, the UK market was dominated by payday loans—high-interest, short-term products that had to be repaid in full on your next salary date. Drafty loans were designed specifically to disrupt this model.

| Feature | Drafty Line of Credit | Traditional Payday Loan |

| Repayment | Flexible (Minimum monthly payment) | Full amount on next payday |

| Interest | Only on the amount used | On the full loan amount |

| Reusability | Use again without reapplying | Must reapply every time |

| Fees | No late or early fees | Often high default/late fees |

By offering a Representative 96.2% APR (variable), Drafty is considerably cheaper than the 1,000%+ APRs often seen in the payday sector, though it remains more expensive than a standard high-street bank loan.

The Application Process: How to Get Started

Applying for Drafty loans is an entirely digital process, optimized for speed in 2026.

-

Check Eligibility: You can use their online tool to see if you are likely to be accepted. This involves a soft credit search, which will not affect your credit score.

-

Provide Details: You’ll need to provide your address history, employment details, and your monthly income (Drafty generally requires a minimum net income of £1,250 per month).

-

Open Banking: To speed up approval, Drafty uses Open Banking to securely verify your income and expenditure.

-

Instant Decision: In most cases, you receive a decision immediately. Once approved, you can draw your first bit of cash instantly.

Eligibility Criteria for Drafty Loans in the UK

To be successful in your application for Drafty loans, you typically need to meet these standards:

-

Age: 18 years or older.

-

Employment: You must be in regular employment (full-time or part-time).

-

Income: A minimum monthly take-home pay of £1,250.

-

Residency: You must be a permanent UK resident with a valid bank account and debit card.

-

Credit History: While Drafty considers those with “less-than-perfect” credit, you cannot currently be in an active IVA or Bankruptcy.

Understanding the Costs: Representative Examples

Transparency is a major part of the Drafty loans brand. Because the interest is daily, the cost depends entirely on how long you keep the money.

Representative Example (Line of Credit):

Assumed Credit Limit: £1,200

Representative APR: 96.2% (variable)

Annual Interest Rate: 69.4% (variable)

Daily Cost: 19p per £100 borrowed.

If you borrow £100 for 30 days, it will cost you £5.70 in interest. If you pay it back after 10 days, it only costs you £1.90. This flexibility is what makes Drafty a popular choice for emergency expenses like car repairs or broken boilers.

The Pros and Cons of Drafty Loans

The Advantages:

-

True Flexibility: You have total control over how much you repay each month (as long as you meet the minimum).

-

Speed: One of the fastest lenders in the UK for emergency cash.

-

Credit Building: Making regular, on-time payments to your Drafty account is reported to credit bureaus, which can help improve your score.

-

No Fee Structure: The lack of late fees is a significant safety net for borrowers.

The Disadvantages:

-

Variable Rates: Because the APR is variable, your interest costs could theoretically increase if market conditions change.

-

Higher than Banks: If you have an excellent credit score, a credit card from a major bank will almost always be cheaper.

-

Temptation to Overspend: Because the money is “always there” once approved, it requires discipline to not treat it as extra income.

Is Drafty Safe? Regulation and Reputation

Yes, Drafty loans are safe. Drafty is a trading name of Gain Credit LLC, which is fully authorized and regulated by the Financial Conduct Authority (FCA) (FRN: 689378). This means they must follow strict rules on affordability and fair treatment of customers.

As of April 2026, Drafty holds an “Excellent” rating on Trustpilot, with thousands of five-star reviews highlighting the ease of the app and the speed of the “90-second” transfer.

Final Thoughts: Should You Apply for a Drafty Loan?

Drafty loans are an ideal solution for UK residents who need a “safety net” rather than a one-off lump sum. The ability to borrow exactly what you need and pay it back as soon as you have the funds makes it one of the most efficient ways to manage short-term cash flow gaps.

However, it is not a long-term solution for chronic debt. If you find yourself relying on your Drafty line of credit every month just to make ends meet, it may be time to seek free debt advice from organizations like StepChange or MoneyHelper.

For those who are financially stable but want a fast, flexible, and fee-free alternative to traditional credit, Drafty loans remain a top-tier choice in the 2026 UK lending market.